Discover more from Fresh Economic Thinking

Why is the rent-to-income-ratio flat?

For decades private renters in many countries have spent roughly the same share of income on housing.

Many housing commentators believe that housing rents should fall as a proportion of income over time. Just like the price of clothes and electronic goods, the market for housing is commonly thought to operate in a way that will gradually make rental prices fall relative to incomes.

If only pesky regulations didn’t get in the way. Or so they say.

Here’s an example.

Consumer economics

As incomes grow, households must spend their additional income on something. Sometimes, they spend a bigger share of their budget on luxury goods, a smaller share of the budget on inferior goods, and for most goods, roughly similar shares.

For example, when incomes rise, households generally buy more clothes or more expensive clothes until they spend roughly the same share of their income on clothes as they did before.

Sometimes, for more luxury items like jewellery or international holidays, the proportion of the household budget spent on these items might rise as income grows.

Where does housing fit in this picture?

There is an element of need when it comes to housing. Just like clothes and food, we can expect that as incomes grow most households spend more on housing rents. How much more depends on the degree to which households choose to substitute towards better quality and more quantity.

The evidence

In many countries where there is widely thought to be a housing crisis, the proportion of household income spent on housing rent in private markets has been roughly constant for three decades.

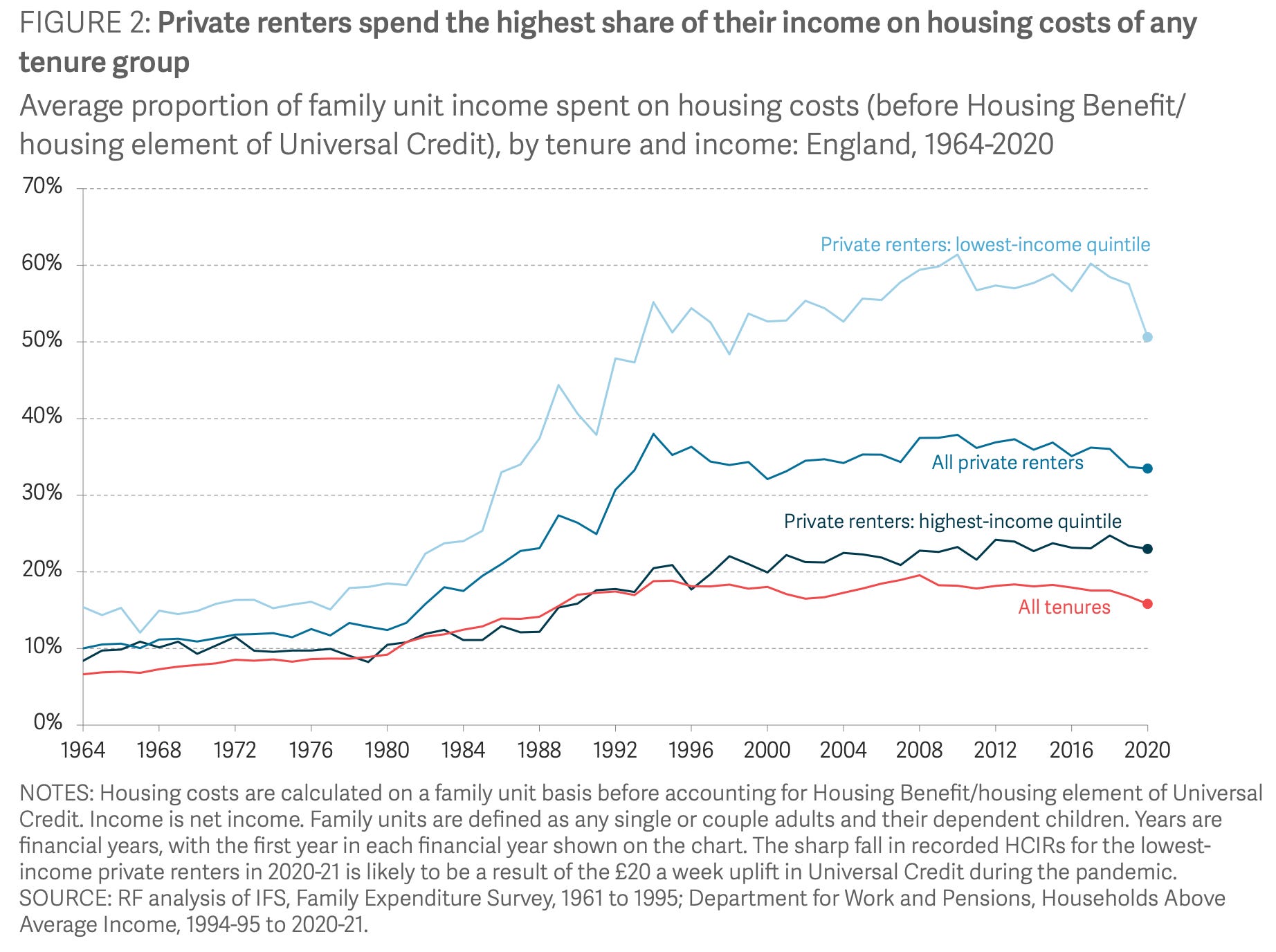

Here’s the situation in England, where the rent-to-income ratio has been flat since the 1990s.1

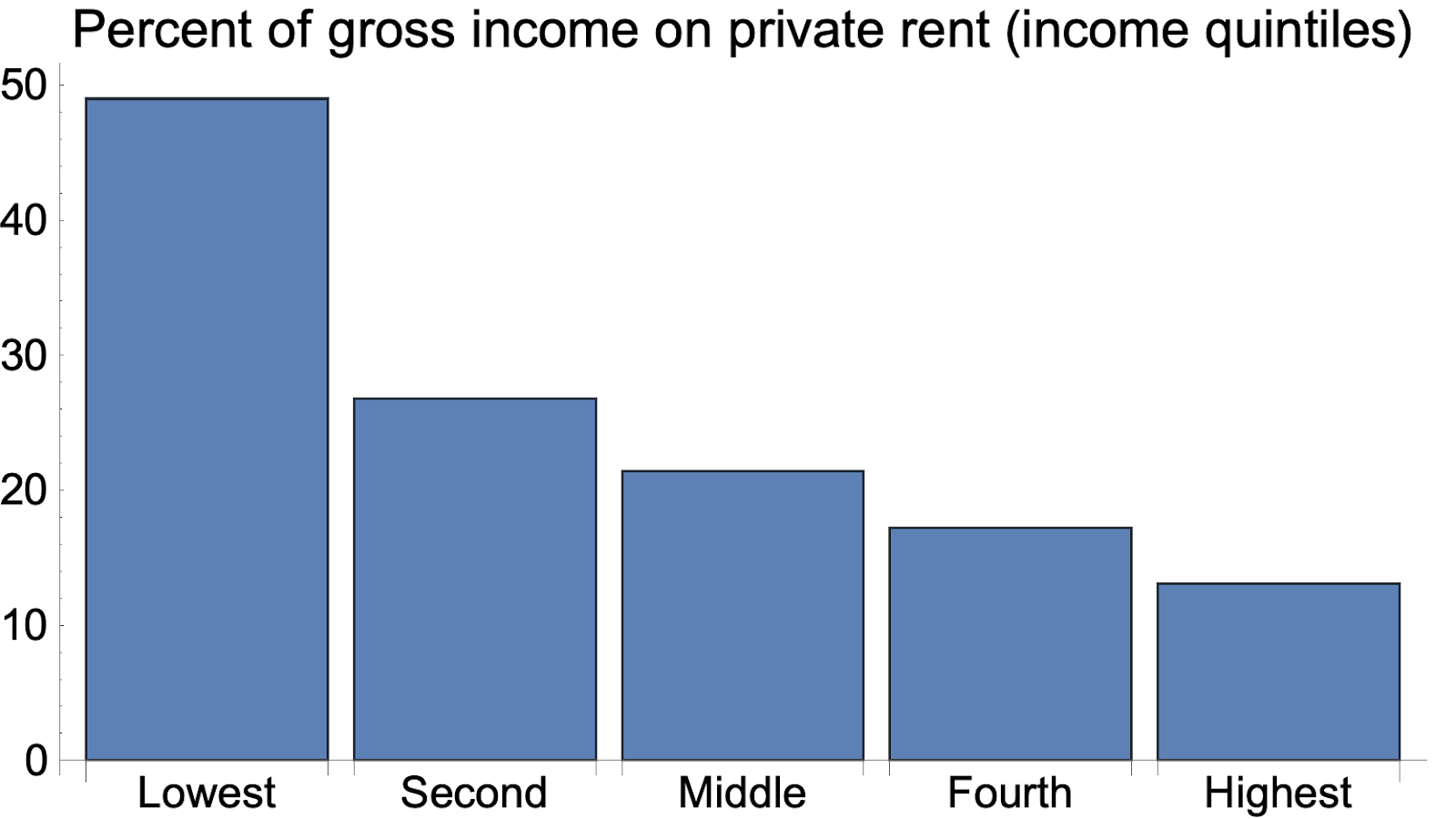

Note that as one household’s income grows relative to all others, they do spend a smaller fraction of their income on housing rents. This is also shown below from Australian data, with the share of income falling from nearly 50% to about 15% as a household moves from the lowest to highest income quintile.

But if we look on average across the market, we see the same decades-long flat line in rent-to-income ratio.

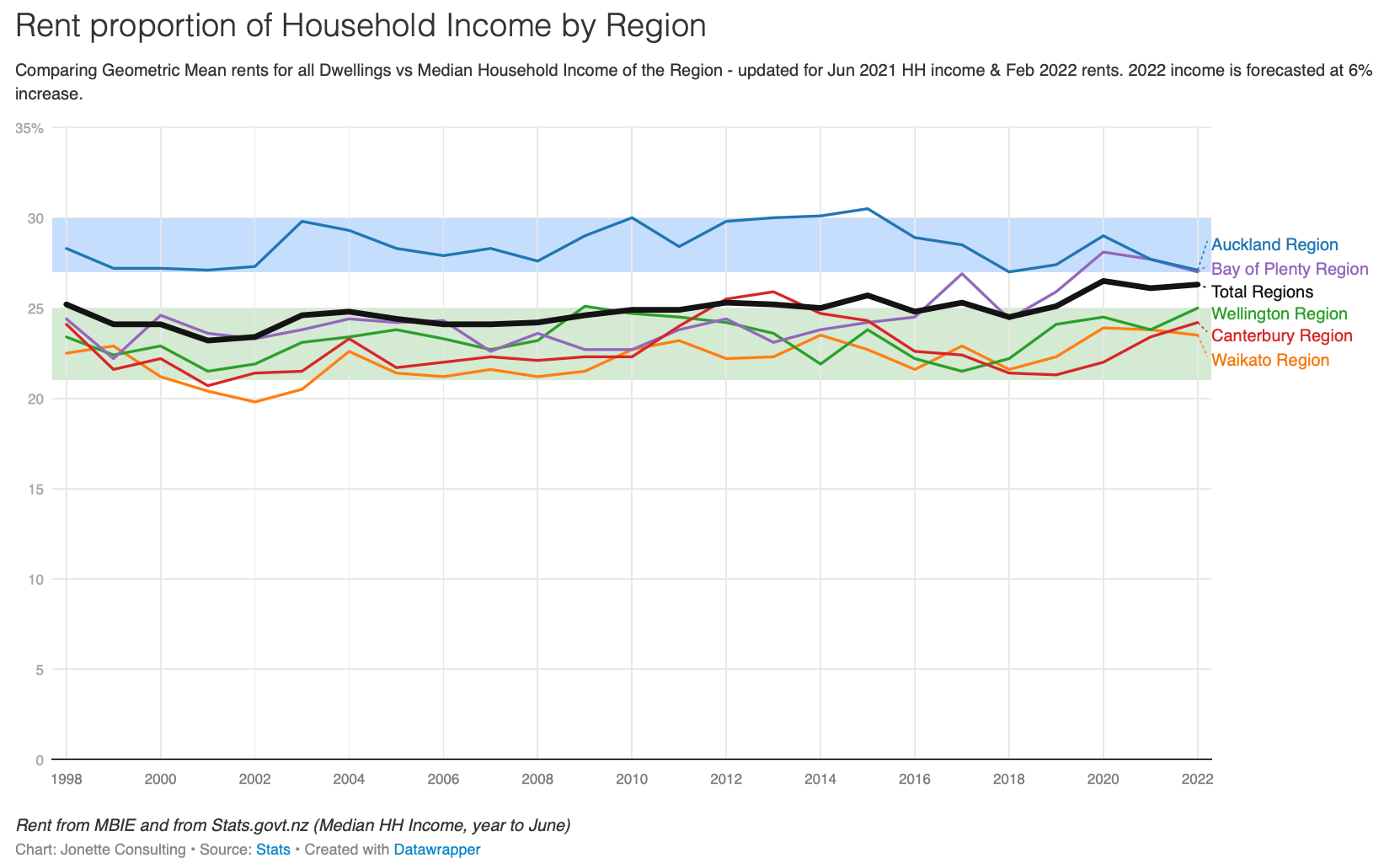

Lastly, we can also see the same pattern in New Zealand since the 1990s.

To be clear, it is true that as one household’s income rises relative to others their rent-to-income ratio falls. But as all incomes rise across the market, the average renter spends the same share of their income on rent.

What if housing rents became cheap?

Would rents stay cheap?

Imagine if rents suddenly become 5% of household incomes on average, down from the typical 20-30%. What then? What mechanism would keep rents there?

I would argue that immediately households would realise they can move or upgrade to a better home or a better location by spending just a little more, say 7% of their income, to outbid others to rent the better home.

This process of spending more on housing to rent a bigger and/or better dwelling would continue until households found that there was no longer a net benefit to them from giving up other goods and services for more or better housing. Ultimately we would be back to exactly the original budget share being spent on housing rents.

The puzzle happened decades ago

In England, the increasing proportion of income spend on private rental housing happened in the 1980s. I understand similar changes happened elsewhere, and I expect to write more about this as I gather better information.

I suspect the lower pre-1980s rent-to-income ratios had something to do with public and council housing options keeping a lid on the private market equilibrium. When you have a cheap outside option, the private market equilibrium shifts. I’ve explained the logic before. Just like central banks manipulate the private pricing of assets by offering an outside option, so too do public housing options shift the private market equilibrium.

However, the change is much larger than I would expect. I sense there are some data inconsistencies in the above England rent-to-income measure. There is more to look into here.

The point is that for going on four decades, the rent-to-income ratio in private rental markets has been flat, and this is what you would expect in a typical market equilibrium for housing.

One of the reasons that the levels of rent-to-income diverge in popular statistics is because of the measures of income being used. For example, sometimes it is gross before-tax incomes, sometimes adjusted for household size, and sometimes net after-tax-and-transfer cash income. Regardless, as long as the income measure is consistent the flat line is usually there.

Subscribe to Fresh Economic Thinking

New ideas and analysis by Dr Cameron K. Murray

Nice post Cam. I think the declining rent share over income quintiles really demonstrates that rent burdens are primarily a problem of inequality. And public housing can combat that for low-income households while also providing the benefits of an outside option.

One thing that's missing with these measures is the size/location/quality of the housing that's being purchased. Where upzoning increases central densities, it can help people move to higher-amenity locations, even while their housing spend doesn't necessarily fall. I wonder whether a [% of income spent on housing & commuting] could be crude improvement on the above measures (and whether those would also be flat)? Or combining them with metrics on average floorspace & time spent commuting?

Part of the difference between the cross-sectional and time-series income elasticity comes from land being a positional good. If my income increases, but no-one else's does, I might move to a better location and pay more rent. If everyone's income increases we can't all move to a better location, and we will just bid rents up.